How HostBooks GST Software can help you become GST Compliant?

October 4, 2018GSTR-3B Filing Process, Eligibility, Due Date & Penalty

October 13, 2018

GSTR-6 is a monthly return that must be submitted by every taxpayer registered as an Input Service Distributor (ISD) under the Goods and Services Tax (GST) system. It is a crucial GST Return for businesses acting as Input Service Distributors, facilitating the seamless distribution of input tax credit among various units or branches within an organization in proportion of usability.

It is a monthly GST return filed to distribute the ITC received by Input Service Distributor among the branches. This blog will explain everything you need to know about GSTR 6. We have explained the detailed step by step process of filing GSTR 6A return in the end.

However, before you start filing GSTR 6 return you should know why GSTR 6 is filed you should know what GSTR 6 is, who is Input Service Distributor, Purpose, due date, late fees and details to be submitted along with it.

Below is the summary of all the sections, you can skip you are confident about one.

| Section | Summary |

|---|---|

| Who is ISD (Input Service Distributor)? | ISD manages input tax credit distribution among branches of a supplier. Only ISDs file GSTR-6.

|

| Purpose of GSTR-6 Form | Facilitates distribution of Input Tax Credit (ITC) among registered ISD branches. Ensures branches can claim ITC for services consumed. |

| GSTR 6 Due Date and Late Fee | The due date for filing GSTR-6 under GST Act is the 13th of next month. delayed filing with Rs 50/day penalty (no penalty for nil return). |

| Details to be filled in GSTR 6 | GSTIN, Legal Name, Return Period, Details of ITC Received, Amendment of Information, Credit/Debit Notes, Distribution of ITC, Total ITC Calculation, Late Fee Details, Verification and Filing. |

| Step by Step GSTR 6 Return Filing | Detailed process including portal login, return period selection, preparing online, generating GSTR-6 summary, input tax credit review, debit/credit notes, distribution of ITC, total ITC calculation, and final submission. |

Who is ISD (Input Service Distributor)?

It’s important to note that only ISD are required to file GSTR 6.

An Input Service Distributor (ISD) in GST is an office of a goods or services supplier that manages the distribution of input tax credits for common services among its branches. It allows the proportional allocation of input tax credits for services to units with distinct GST identification numbers but the same PAN.

- 1. Scope and Limitations

- Applicable only to input services, not goods.

- Used by companies with a central office and multiple registered units.

- 2. Registration and Compliance

- Requires separate GST registration (no threshold).

- Issues ISD invoices and files monthly returns (Form GSTR-6).

- 3. Credit Distribution

- Credit Distribution is Based on the proportionate turnover of each unit.

- 4. Reverse Charge Mechanism

- Cannot accept invoices under reverse charge.

- Must register separately for handling reverse charge supplies.

Purpose of GSTR 6 Form

The primary purpose of GSTR-6 is to facilitate the distribution of Input Tax Credit (ITC) among the various units or branches of a business that are registered as Input Service Distributors (ISD) under the Goods and Services Tax (GST) regime.

As the branches Consume the services, but the invoice is sent to the central department to be cleared. In this case the GST ITC is provided to the head office as both the ISD and branches have different GSTIN under the same PAN.

Now the ISD must distribute the Input Tax Credit for the GST paid on services consumed by the branches. To allow the branches to claim the ITC, the head office distributes the ITC proportionately by filing GSTR-6.

Details to be Filled in GSTR 6

| Details | Explanation |

|---|---|

| 1. GSTIN | Goods and Services Taxpayer Identification Number of the Input Service Distributor. |

| 2. Legal Name | Legal name of the Input Service Distributor. |

| 3. Return Period | The specific month and year for which the return is being filed. |

| 4. Details of Input Tax Credit (ITC) Received for Distribution |

|

| 5. Amendment of Information Furnished in Earlier Returns in Table 3 |

|

| 6. Credit Notes/Debit Notes Received |

|

| 7. Distribution of Input Tax Credit for ISD Invoices & ISD Credit Notes |

|

| 8. Redistribution of ITC Distributed in Earlier Returns |

|

| 9. Total ITC Available and Eligible ITC | Ineligible ITC Distributed |

| 10. Late Fee Details | Late Fee for the return period |

| 11. Verification and Filing | Declaration – Authorized Signatory |

GSTR 6 Due Date and Late Filing Fee

The due date for filing GSTR-6 under the Goods and Services Tax (GST) Act is filed the 13th of next month.

For the month of April 2023, the return should be filed on or before 13th May 2023.

The late fee for GSTR 6 is Rs 50/Day (₹ 25 CGST and ₹ 25 SGST). However, there is no penalty for nil returns.

GSTR 6 Applicability

- GSTR-6 contains the complete details of all documents issued in favor of distribution of Input Tax Credit among the branches of the organization and the nature of distribution of credit and tax invoice on which credit is received.

- This must be filed by every ISD even if it is a NIL return.

Step by Step Guide to File GSTR-6 on the GST Portal

Following the below steps GSTR-6 can be filed online on the GST Portal easily and quickly.

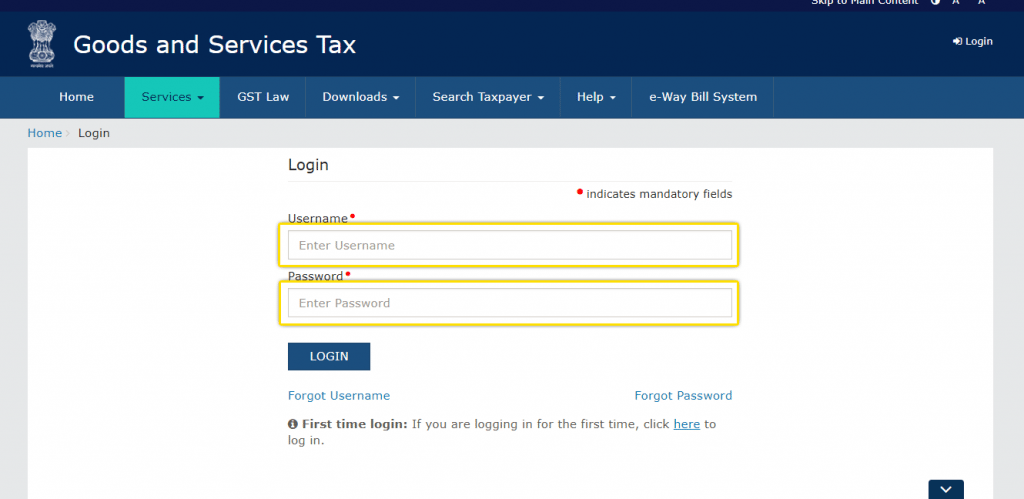

Step 1: Firstly visit the GST common Portal and then enter ‘User name’ and ‘password’ and now click on the ‘LOGIN’ button to proceed to your account.

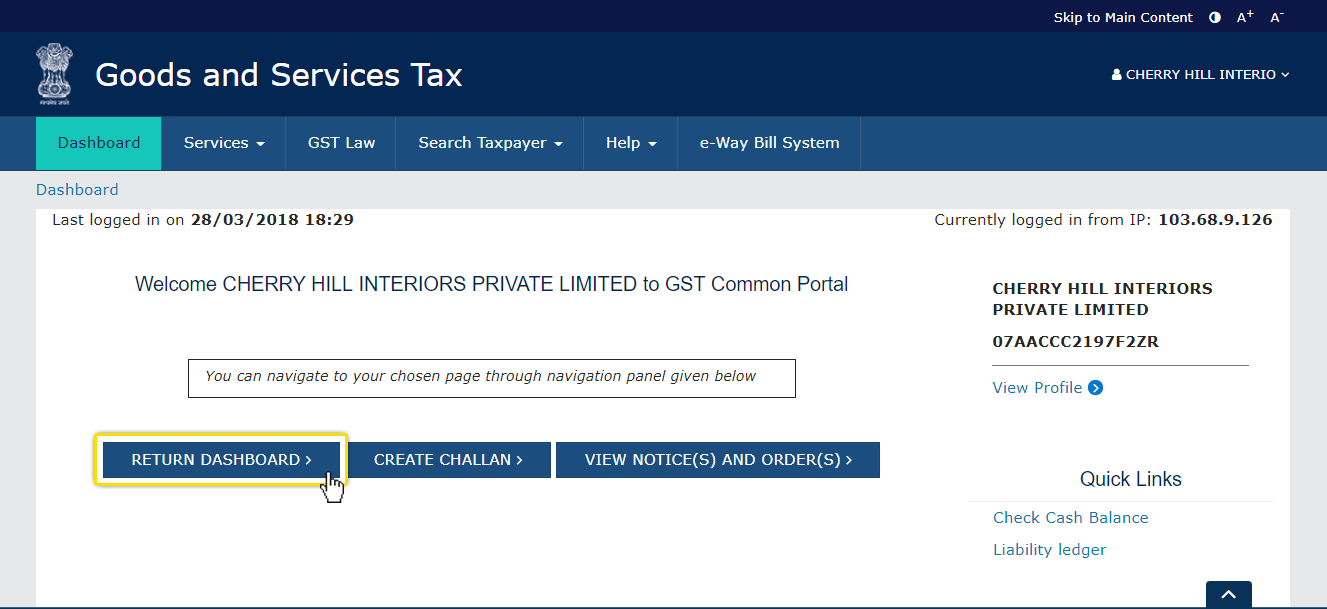

Step 2: A welcome message will be shown and now click on the ‘RETURN DASHBOARD’.

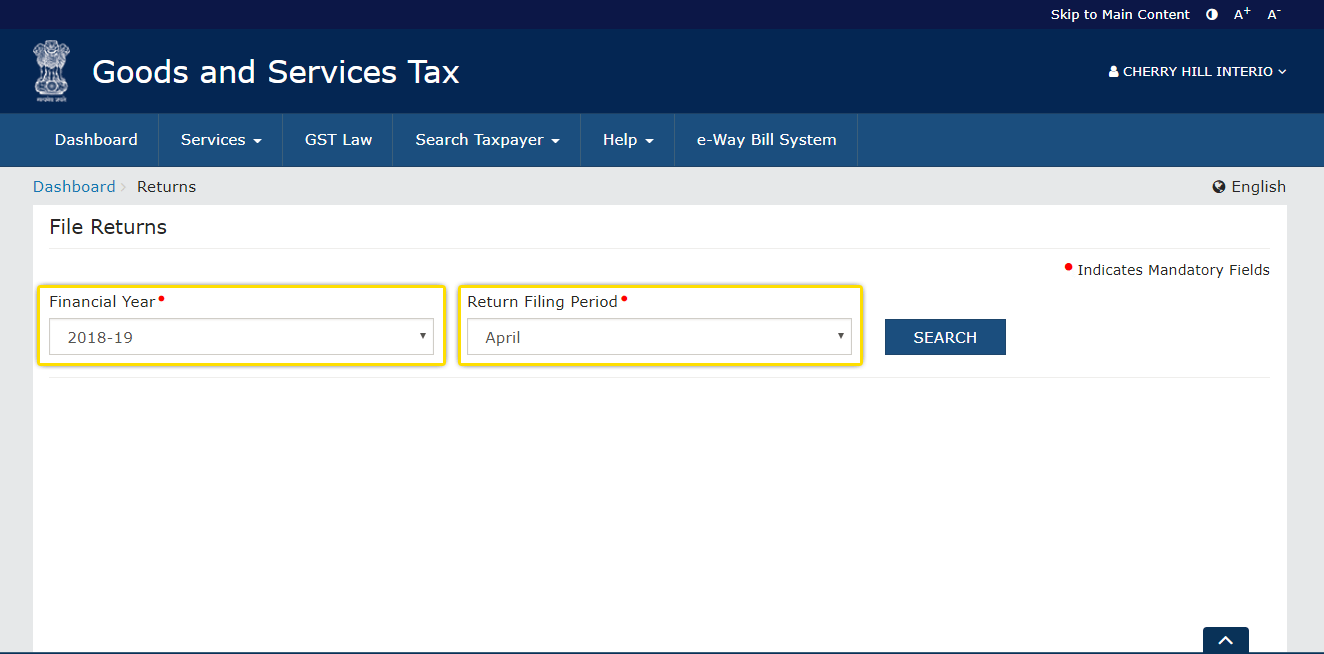

Step 3: From the dropdown option, choose the appropriate ‘Financial Year’ and then the ‘Return Filing Period’ (i.e. month) for which GSTR-6 has to be filed, and now click on the ‘SEARCH’ button.

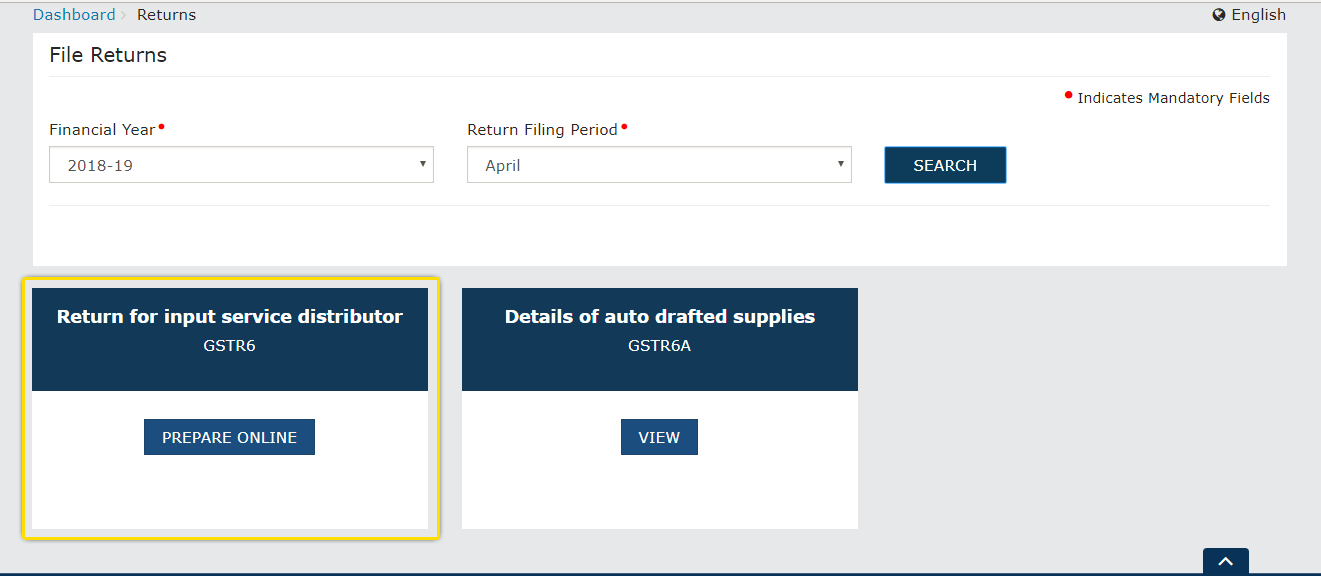

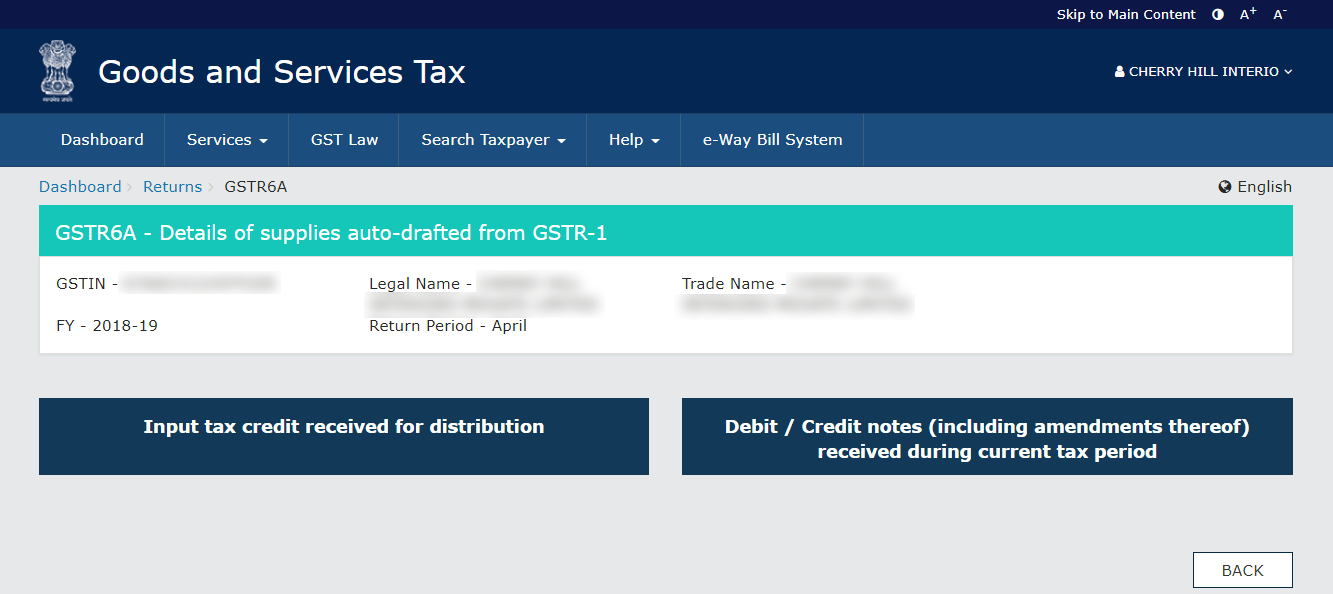

Step 4. By clicking on the ‘PREPARE ONLINE’ button select ‘Return for input service distributor GSTR6’. On the right, there is one more option ‘Details of auto drafted supplies GSTR6A’. It is auto-generated GSTR-6A (only to be viewed by the user).

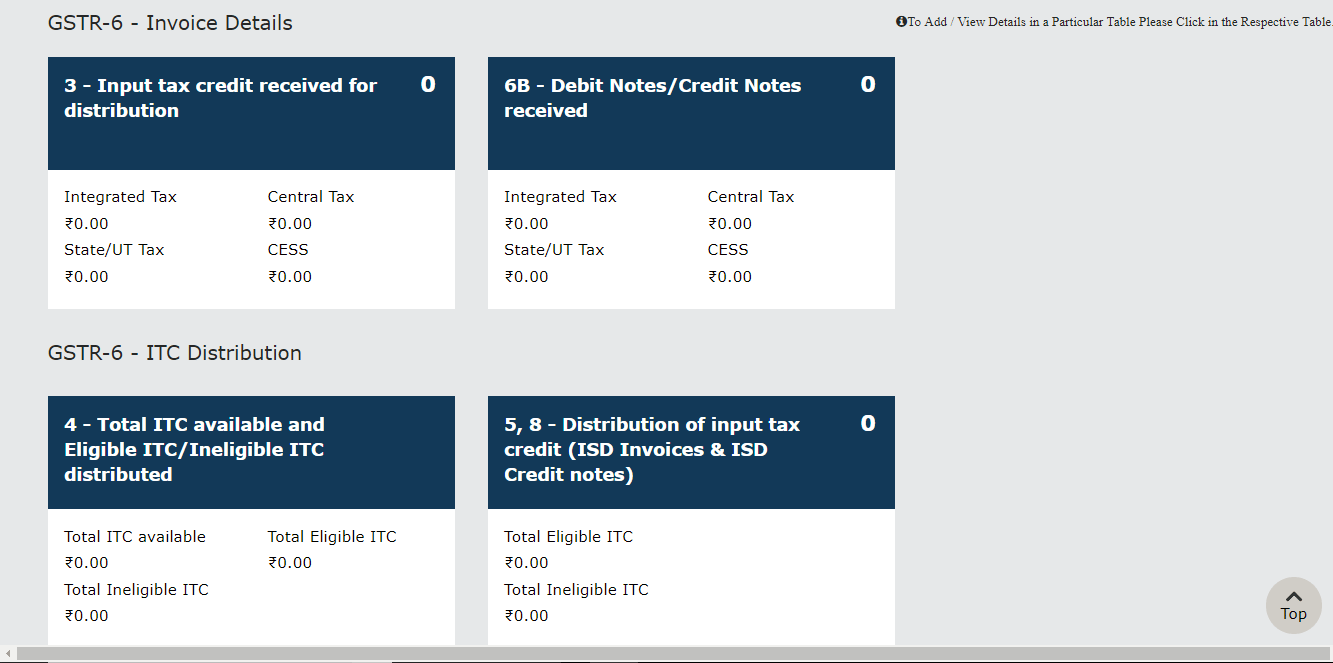

Step 5: One can see the invoice details and distribution of input tax credit after clicking GSTR- 6.

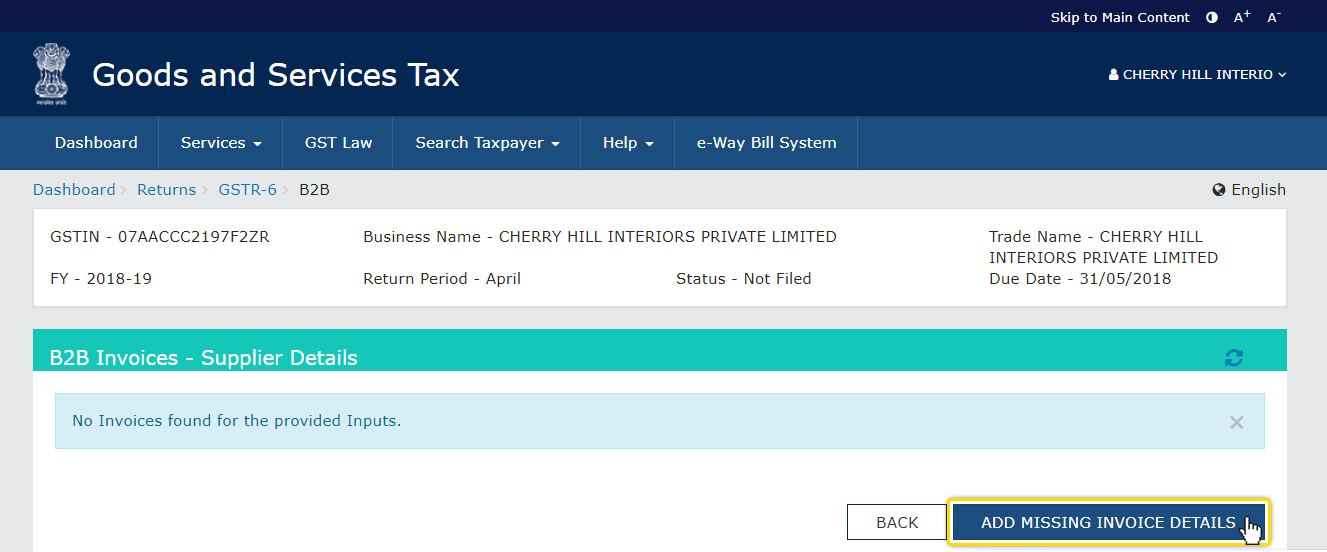

Step 6: Now click on ‘3 – Input Tax Credit received for distribution’ under the head ‘Invoice Details’. A new page will be displayed. And, click on the ‘ADD MISSING INVOICE DETAILS BUTTON’.

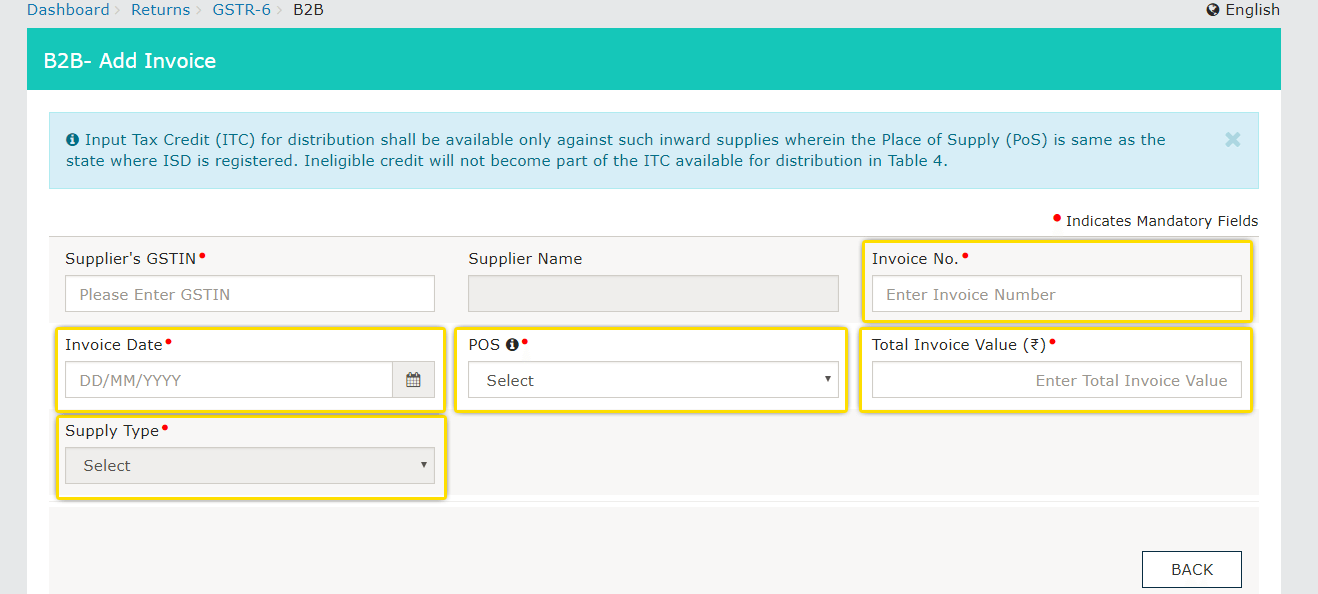

Step 7: All the details like ‘Supplier’s GSTIN’, ‘Supplier Name’ will be appeared automatically while ‘Invoice no.’, ‘Invoice Date’, ‘POS’, ‘Total Invoice Value’ and ‘Supply Type’ needs to be provided by the user.

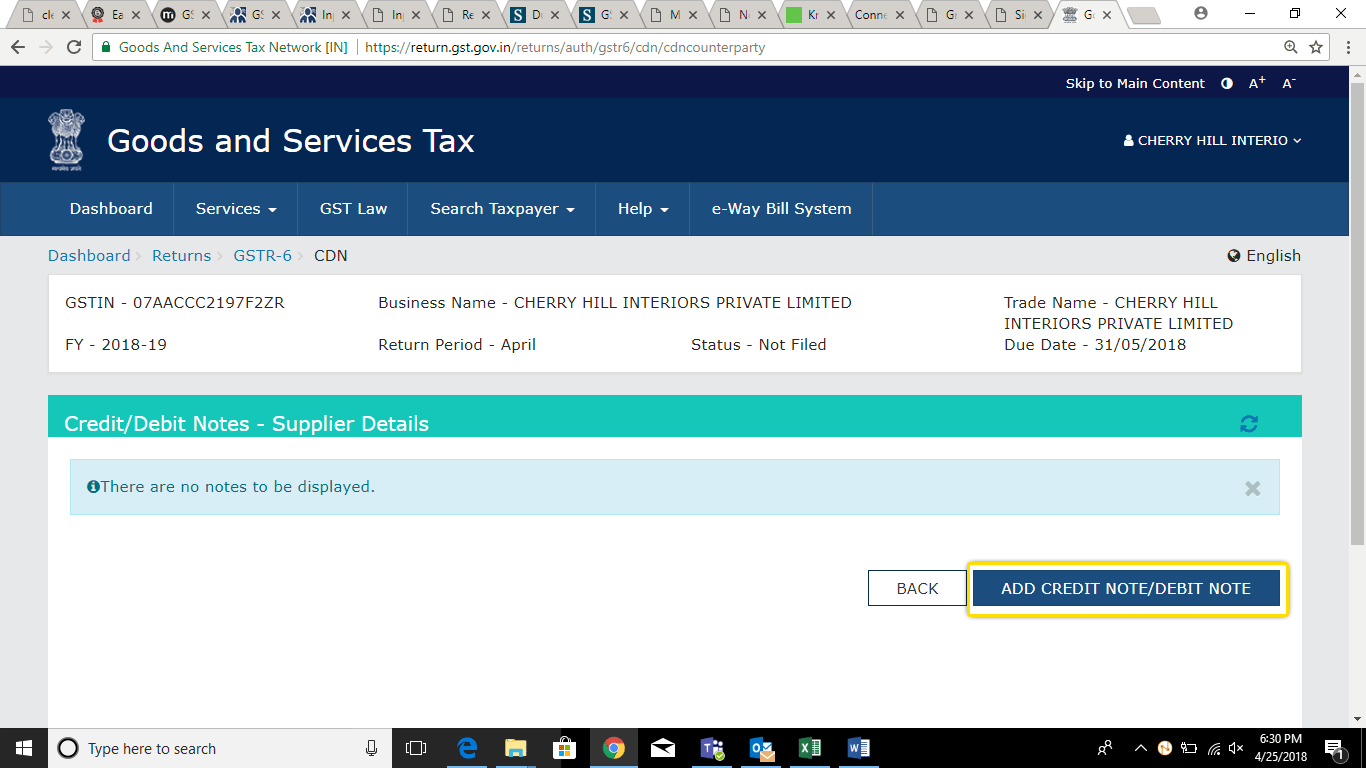

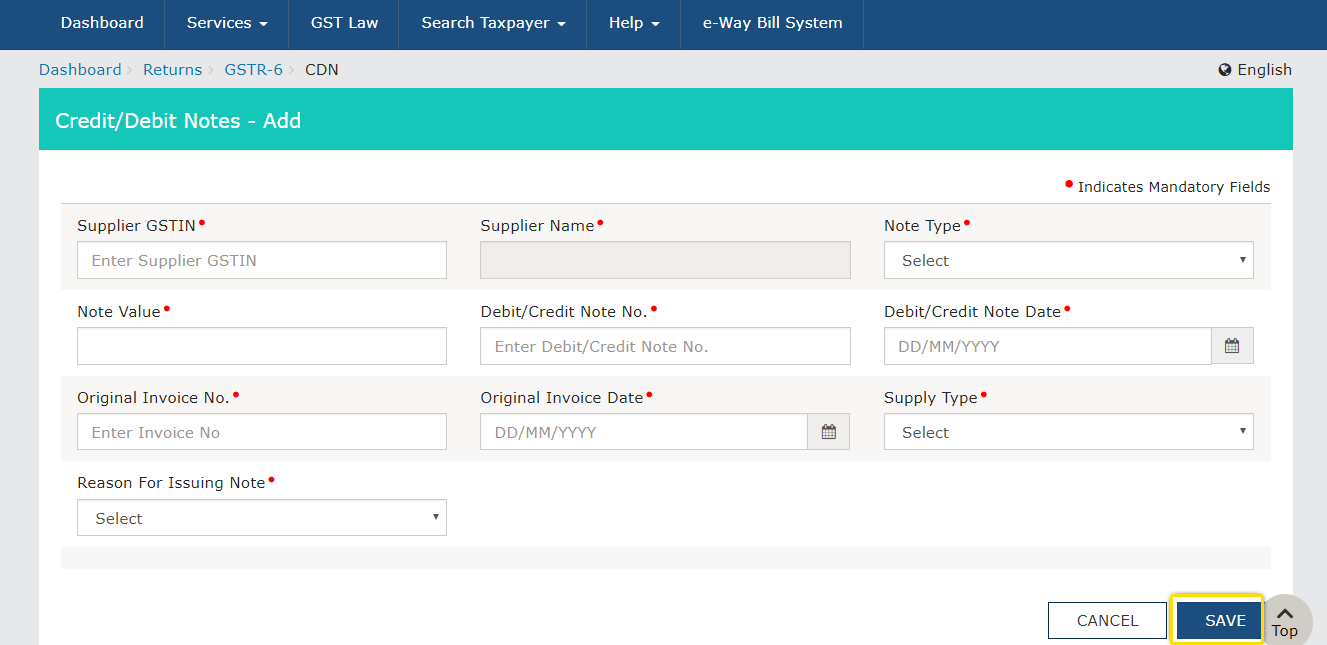

Step 8: Now click on the ‘BACK’ for viewing the page displayed during ‘Step 5’. Here choose the box titled ‘6B – Debit Notes/Credit Notes received’. And, now click on ‘ADD CREDIT NOTE/DEBIT NOTE’ button.

Step 9: Details of credit note with ‘Supplier GSTIN’, ‘Supplier Name’, ‘Note Type’ (debit/credit note) ‘Note Value’, ‘Debit/Credit Note No.’, ‘Debit/Credit Note Date’, ‘Original Invoice No.’, ‘Original Invoice Date’, ‘Supply Type’, ‘Reason For Issuing Note’ needs to be filled by the user himself / herself. And then, click on ‘SAVE’. Now the user will again land to the menu displayed in ‘Step 5’.

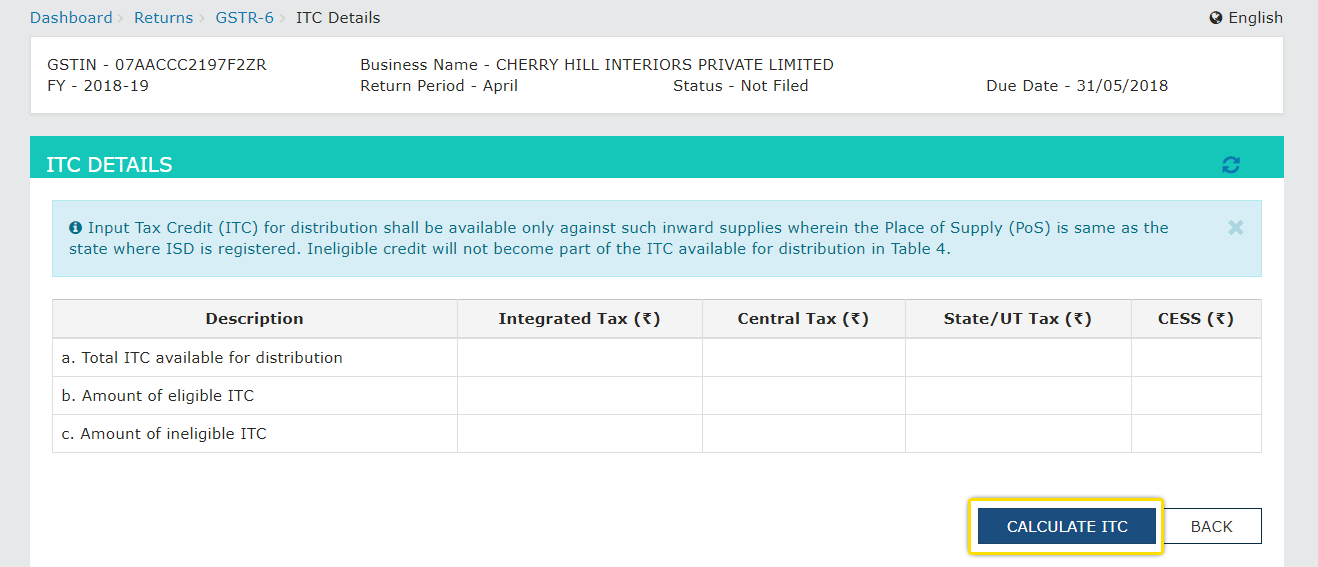

Step 10: Select the box ‘4 – Total ITC available and Eligible ITC/Ineligible ITC distributed’. Fill up all the details asked in the boxes and then click on ‘CALCULATE ITC’.

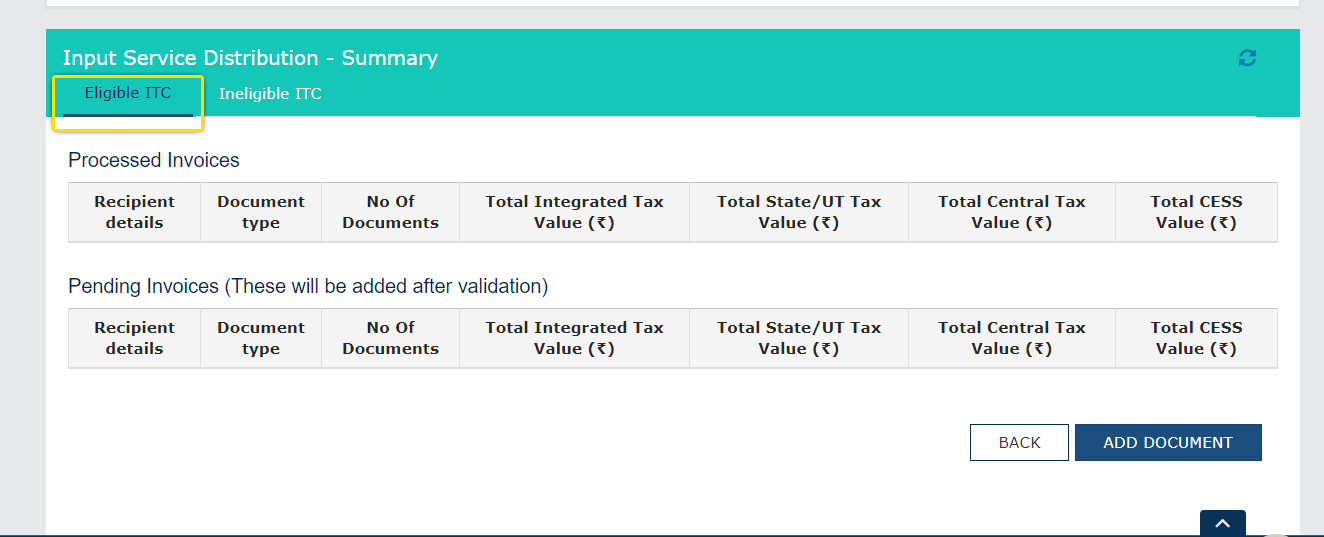

Step 11: Select ‘Eligible ITC’ and one can see the amount which is distributed to the branches and detailed summary of all the invoices. This comes up with any of the two options –

- ‘Processed invoice’ – where all the details are accepted.

- ‘Pending invoice’ – details which are still in process and getting validated.

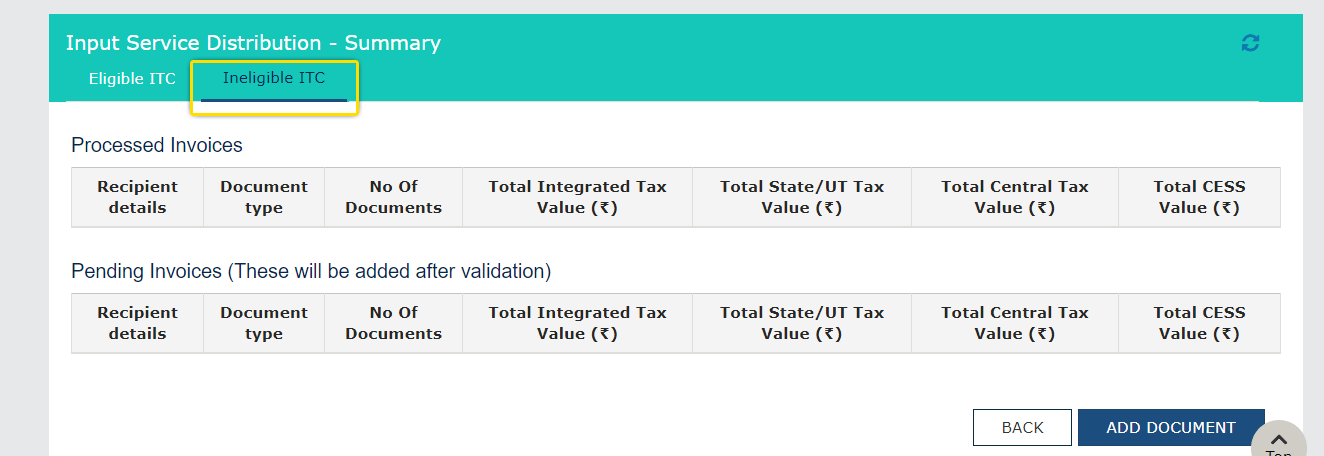

Step 12: Select ‘Ineligible ITC’, a detailed summary of the amount distributed to various branches (which is ineligible) will be displayed. Again this may show any of the two options –

- ‘Processed invoice’ – where all the details are accepted.

- ‘Pending invoice’ – details which are still in process and getting validated.

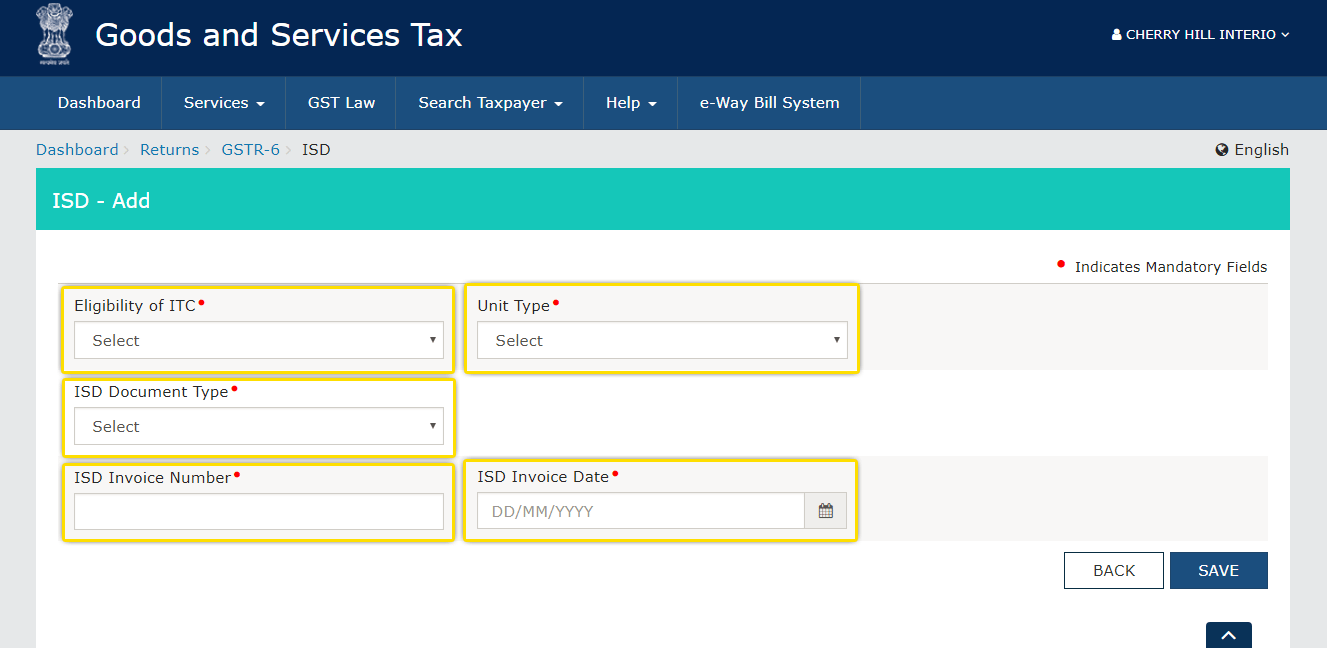

Step 13: Details like ‘Eligibility of ITC’, ‘Unit type’, ‘Document type’, ‘ISD invoice number’ and ‘ISD invoice date’ needs to be filled up appropriately. And now, proceed by clicking on ‘SAVE’.

Step 14: Form GSTR-6 gets auto-populated. And details of Input credit received for distribution and debit/credit notes received during current period is reflected of its own in the form.

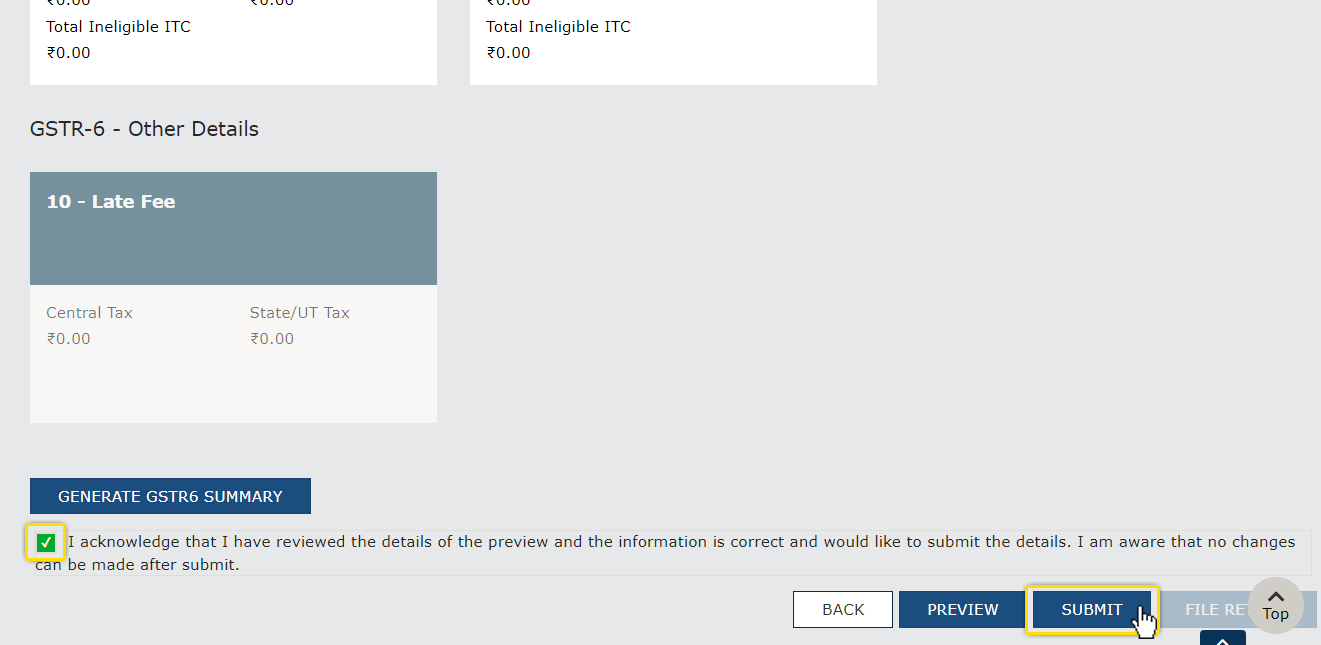

Step 15: Now click on the last option ‘10 – Late Fee’ under heading ‘GSTR-6 – Other Details’. After filling up all the details appropriately, click on the checkbox under heading ‘GENERATE GSTR-6 SUMMARY’ and finally click on ‘SUBMIT’ and then on ‘FILE RETURN’ to complete the filing process of GSTR-6.

FAQs About GSTR 6

What is GSTR-6?

GSTR-6 is a monthly return that must be filed by every taxpayer registered as an Input Service Distributor (ISD) under the Goods and Services Tax (GST) system. This return facilitates the distribution of input tax credit among various units or branches within an organization.

What is the difference Between GSTR-1 and GSTR-6?

GSTR-1 is a return for outward supplies filed by regular taxpayers, providing details of sales. On the other hand, GSTR-6 is specific to Input Service Distributors, focusing on the distribution of input tax credit among different units or branches.

What is table 6 in GST?

In GSTR-6, Table 6 is likely referring to a specific section or part of the return where details related to input tax credit distribution are provided. The exact details in Table 6 would include information about credit distribution for ISD invoices and ISD credit notes.

How do I view GSTR 6?

To view GSTR-6, taxpayers can log in to the official GST portal, navigate to the ‘RETURN’ section on the dashboard, select the appropriate financial year and return filing period, and then access the GSTR-6 form. The return can be viewed and edited before submission.

Is GSTR-6 Mandatory?

Yes, GSTR-6 is mandatory for businesses registered as Input Service Distributors (ISD) under GST. It is a monthly return, and non-compliance may lead to penalties and legal consequences.

What is the limit of GSTR-6?

As of my last knowledge update in January 2022, there is no specific turnover threshold for GSTR-6. However, businesses that qualify as Input Service Distributors and have multiple registered units are required to file GSTR-6.

Who is Eligible for GSTR-6?

Businesses registered as Input Service Distributors (ISD) under GST are eligible to file GSTR-6. An ISD is an office of a goods or services supplier that manages the distribution of input tax credits for common services among its branches.

Team@HostBooks

Try HostBooks

SuperApp Today

Create a free account to get access and start

creating something amazing right now!

3 Comments

It is very helpful blog article on gstr-6 return filing, once again thank you. keep it up

Dear Madam, We have taken GSTR-6 registration. if Service vendor not filed GSTR-1 and GSTR-3B. What action should be taken?

• When service provider has not filed GSTR-1, than data doesn’t show in your GSTR-6A. Therefore, you are not eligible for ITC as per section 16 of CGST Act, 2017

• In the given case, supplier has not filed GSTR-1 & GSTR-3B. You can directly approach your services provider to file GSTR-1 return to claim ITC on services received.

• Action taken by you is a direct approach to your service provider to file GSTR-1, otherwise you can hold GST tax amount of the service provider and pay held amount after showing in your GSTR-6A.